5 Strategies to LOWER Taxes (Over Your Lifetime)

It’s the most wonderful time of the year… for the IRS. It’s tax season! While it may be joyous for the government, it’s groan-inducing for most people. We all have one thing on our minds: “How do I pay less taxes!” We’re going to cover five strategies to lower taxes over your lifetime.

Last Year’s Taxes vs. Lifetime Taxes

The strategies we cover today focus on saving taxes over your lifetime. Far too many people focus on preparing and filing last year’s taxes. But by the time the year ends and we’re in tax preparation mode, we’ve lost access to most of the available tax-saving strategies.

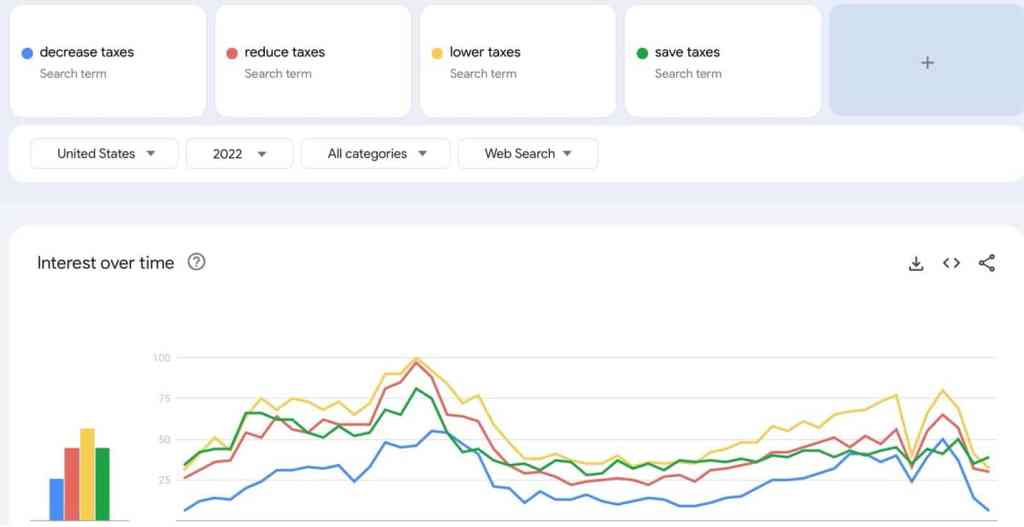

This is how most people operate: reacting to taxes of the past rather than reducing taxes of the future. Look at this Google Trends graph of search terms related to lowering taxes. (If you’re listening to this on the RetireMentorship Podcast, switch to the Vodcast or video podcast feed to see what we’re looking at.)

Over a year, interest in reducing taxes starts climbing in January as Tax season approaches and peaks the week of April 15th! It then drops off significantly over the summer and builds more over November and December (with drops for Thanksgiving and Christmas). The people who search at the end are proactive, trying to figure out what they can do before the year ends to reduce taxes. But most people are looking too late.

Let’s stop merely looking at last year’s taxes and start preparing for what we will pay in taxes over our lifetimes.

Tax Deduction vs. Tax Credit

Before we discuss the strategies, let’s clarify the difference between a Tax Deduction and a Tax Credit. The difference lies in how they reduce your tax liability (the amount of taxes you owe).

Tax Deduction

A tax deduction lowers your taxable income, which is the income subject to taxation. By reducing your taxable income, deductions indirectly lower the amount of taxes you owe.

For example, if your taxable income is $100,000 and you claim a $5,000 deduction, your taxable income is reduced to $95,000. The actual tax savings depend on your tax bracket. If you’re in the 22% tax bracket, this deduction will save you $1,100 in taxes ($5,000 × 0.22).

Tax Credit

A tax credit, on the other hand, directly reduces your tax liability on a dollar-for-dollar basis.

For instance, if you owe $5,500 in taxes and claim a $1,000 tax credit, your tax bill drops to $4,500. Some tax credits are even refundable, meaning they can result in a refund if they reduce your tax liability below zero.

Key Difference

- Deductions lower your income before taxes are calculated.

- Credits reduce the actual taxes you owe.

Imagine you owe $3,000 in taxes.

- A $1,000 deduction saves you $220 if you’re in the 22% tax bracket.

- A $1,000 credit reduces your tax bill by the full $1,000.

In short, while deductions reduce the amount of taxable income, credits directly cut your tax bill, often making credits the more valuable of the two.

Five Strategies to Lower Taxes

This is not a comprehensive list, nor will we go into all the details. But it will help you think bigger, and at the end of the post, I’ll give you some actions you can take today to stick it to the IRS tomorrow.

Strategy 1: Pay College, Not the IRS

The first strategy is a Tax Credit, while the others involve reducing taxable income and tax liability.

Many of you may have children or grandchildren who are or will be attending university. While some people have pre-mediated means to help with their family members’ education expenses, many don’t. I’ve seen far too many instances of folks paying extra taxes while their students rack up extra student loans.

Folks, pay for college, not the IRS. Take advantage of the American Opportunity Tax Credit.

The AOTC is designed to make college more affordable by providing up to $2,500 per year in tax credits for eligible students. It covers tuition, fees, and course materials essential for academic success.

Here’s how it works: 100% of the first $2,000 in qualified expenses is credited, plus 25% of the next $2,000. Which option would you like:

- Pay $2,500 in extra taxes for the government to squander and let your student acquire $4,000 in extra student loans.

- Pay only $500 in extra taxes and $2,000 to the university, so your student only acquires $2,000 in extra student loans.

- Pay $0 in extra taxes and $4,000 to the college ($1,500 more out of your pocket, but less in taxes), so your student acquires no extra student loans.

The AOTC can only be used once per year per student. This means only one person can claim it per student but can also claim it for multiple students. With up to $10,000 in tax credits per student, if you have many kids or grandkids, this can be worth tens of thousands in tax savings with some proactive planning. Other restrictions apply, so ask your tax planner about incorporating this strategy.

Strategy 2: Compound Your Triple Tax Advantage!

Do you have a Health Savings Account? Have you invested it? If not, double it and compound your triple tax advantage.

A Health Savings Account (HSA) is a tax-advantaged savings account designed to help you pay for qualified medical expenses. To open one, you must be enrolled in a high-deductible health plan, which means you pay lower monthly premiums but cover more out-of-pocket costs before insurance kicks in.

Here’s how it works: You contribute pre-tax dollars to your HSA, which reduces your taxable income. The account grows tax-free. These funds can then be used tax-free for eligible health expenses, like doctor visits, prescriptions, or even dental and vision care.

Most people know these, but they stop at a health savings account. They put their triple-tax-free funds into a savings account earning 0% interest just to get the deduction. Many also only contribute as much as they will spend on medical expenses that year. But that’s a mistake.

Don’t treat your HSA like a transactional checking account. Get a Health Savings Brokerage Account and invest your HSA! Max it out every year and invest what you don’t plan on spending that year (and perhaps all of it). By doing this you are compounding the triple-tax-free effect and giving your future self options for withdrawals to minimize future taxes.

I generally recommend to my clients this order of savings:

- Contribute up the to the match in your Employer’s 401(k)

- Max out an HSBA

- Explore Roth IRAs vs. additional 401(k) contributions

Did you catch that? Maxing out and investing an HSA is better than a Roth IRA. But you must invest it, or the strategy doesn’t work.

There are other requirements and stipulations regarding HSAs, and there is a lot to know about investing, so make sure you ask your tax planner if this strategy is right for you.

Strategy 3: Bundle Your Deductions

After the Tax Cuts and Jobs Act effectively doubled the Standard Deduction, most people claim it yearly rather than itemizing deductions. But for many, defaulting to the Standard Deduction is a mistake. With proactive planning, you can minimize your taxes by bundling your deductions.

Deduction bundling is a tax strategy where you consolidate or “bundle” deductible expenses into a single tax year to maximize the benefit of itemizing deductions rather than taking the standard deduction. This approach is particularly useful when total itemized deductions are close to the standard deduction threshold.

How Deduction Bundling Works

Instead of spreading deductible expenses, like charitable donations, property taxes, or medical expenses, over multiple years, you concentrate them into one tax year so that the total of your itemized deductions surpasses the standard deduction, allowing you to reduce your taxable income more effectively.

Suppose the standard deduction is $30,000 for a married couple filing jointly and that they have the following itemizable deductions:

- State Taxes $5,000

- Property Taxes: $2,500

- Mortgage Interest: $4,500

- Charitable Donations: $12,000

- Total Itemized Deductions: $24,000

With $24,000 in itemizable deductions, this couple would take the higher $30,000 standard deduction every year.

However, they could “bundle” deductions into one year. Property tax bills are often issued in December and payable in the following year. However, if they already paid last year’s property taxes in January of this year, they could pay next year’s taxes in December of this year as well, effectively sliding two years of property taxes into one year. If they give $1,000 monthly and have the funds, they could pre-give all $12,000 of next year’s giving in December. Thus, over two years, their deductions would look like this:

No Planning W/Planning W/Planning

Annually This Year Next Year

- State Taxes $5,000 $5,000 $5,000

- Property Taxes: $2,500 $5,000 $0

- Mortgage Interest: $4,500 $4,500 $4,200*

- Charitable Donations: $12,000 $24,000 $0

- Total Itemized Deductions: $24,000 $38,500 $9,200

- Standard Deduction $30,000 $30,000 $32,000*

*Because paying down the mortgage reduces mortgage interest and the Standard Deduction increases yearly, it generally makes sense to pull future expenses into the current year rather than push them forward into the next year.

By bundling deductions, this couple would Itemize Deductions this year and claim the Standard Deduction next year. In this example, they claim an extra $8,500 in deductions this year and the same deduction they would have claimed next year. At 22% Federal Income Tax, that’s almost $2,000 in savings.

Why is this a lifetime tax-saving strategy? You can bundle deductions every other year! If you add that up, you could save tens of thousands of dollars in taxes! Your tax planner can help you set up this strategy.

Strategy 4: Give to Charities, Not the IRS

Tax savings become even easier in retirement with the Qualified Charitable Distribution (QCD). A QCD allows individuals aged 70½ or older to donate directly from their traditional IRA to a qualified charity. The key benefit? The donation is tax-free.

Normally, when you withdraw funds from an IRA, the amount is added to your taxable income. But with a QCD, the money goes straight to the charity, bypassing your taxable income altogether. And because charities aren’t taxed, the money is never taxed!

Even better, QCDs can count toward your required minimum distributions (RMDs), starting at age 73 or 75. This means you can fulfill your RMD obligation while supporting causes you care about without increasing your tax bill.

The annual limit for QCDs is $100,000 per person, so it’s a great tool for substantial giving.

Using a QCD reduces your taxable income, potentially lowering your overall tax burden and making a meaningful impact on your favorite charities. It’s a win-win for your finances and philanthropy!

Remember that this is available when you hit age 70 ½, not RMD age. I see many people over this age but not yet RMD age giving to charity from their bank account and paying taxes on their IRA withdrawals. Flip that around and give directly out of your IRA. You can set up pre-planned gifts or, if you’re IRAs are at the right custodian, you can get a checkbook for your IRA and write checks to charities right out of that account. Just make sure you have cash available to cover the gift!

Ask your tax planner if you should switch to QCDs or postpone charitable giving until you can utilize them.

Strategy 5: Proactively Pay Less Taxes

Lastly, we have two choices regarding our retirement accounts and taxes. We can wait around and reactively pay extra taxes or proactively pay taxes now to reduce lifetime taxes.

The most common method for this is the Roth Conversion. In short, we move money from our Pre-Tax IRA to our Post-Tax Roth IRA. This allows us to pay the taxes now and let that money grow tax-free forever! This is a big topic; we’ve covered it in other places, which we’ll link to in the description. Most importantly, ask your tax planner if a Roth Conversions Strategy is right for you. If you have a good one, they will have already told you.

Tax Preparation vs. Tax Planning

You may have noticed that after each strategy, I recommended asking your tax “planner” for help, not your tax “preparer” or “professional.” A “tax professional” means anyone working on taxes for pay. A “tax preparer” is someone who prepares and files taxes. Neither of those titles indicates that they have the competency or capacity to help you with tax strategies.

I recommend that you work with a tax planner. These folks have the knowledge and skills to help you plan and execute these and many other tax-saving strategies. Tax preparation looks at last year’s taxes, hunting for deductions and credits, and shows what you owed for last year. Tax planning looks ahead to the coming year and decades and hunts for strategies that can reduce what you owe over your lifetime. We’ll pay the IRS every dime we owe them, but let’s not leave them a tip.

Get Tax Planning

My firm, La Crosse Financial Planning, has several tax planners. We are Fee-only Fiduciary Certified Financial Planners, meaning we have the expertise to advise and guide you on all your finances without selling any products. Further, a number of us are also Enrolled Agents, the federal license to file taxes and represent taxpayers before the IRS. Here’s what this means:

- We can prepare and file your taxes for last year.

- We can evaluate your situation and recommend tax savings strategies for next year and beyond.

We offer basic Tax Preparation to people looking for help for last year and a premium Tax Planning service to anyone looking to be proactive.

Even if you already have a “Financial Advisor,” you may want to get some tax planning. If your CPA tells you to ask your Financial Advisor, and your Financial Advisor keeps saying, “I can’t give tax advice; go ask your CPA,” it’s time to get a Tax Planner. We can connect the two in a world of siloed professionals.

Take Action!

Go to LaCrosse.tax to explore our Tax Prep and Tax Planning options. We work with people locally and remotely nationwide and specialize in working with folks over age 50.

Our Tax Planning will look at your broader situation, show you how much you are likely to pay in taxes over your lifetime, and provide strategies to reduce those taxes. You’ll get a tax planning meeting with an interactive presentation and a 1-2 page plan with results and recommendations.

Go to LaCrosse.tax or follow the link in the description to schedule your services. I hope these five strategies to lower taxes over your lifetime have sparked some ideas. But ideas are worthless without action. So be proactive and get the guidance you need to keep more of what’s yours.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.