Can I Make A Deductible Contribution To My HSA?

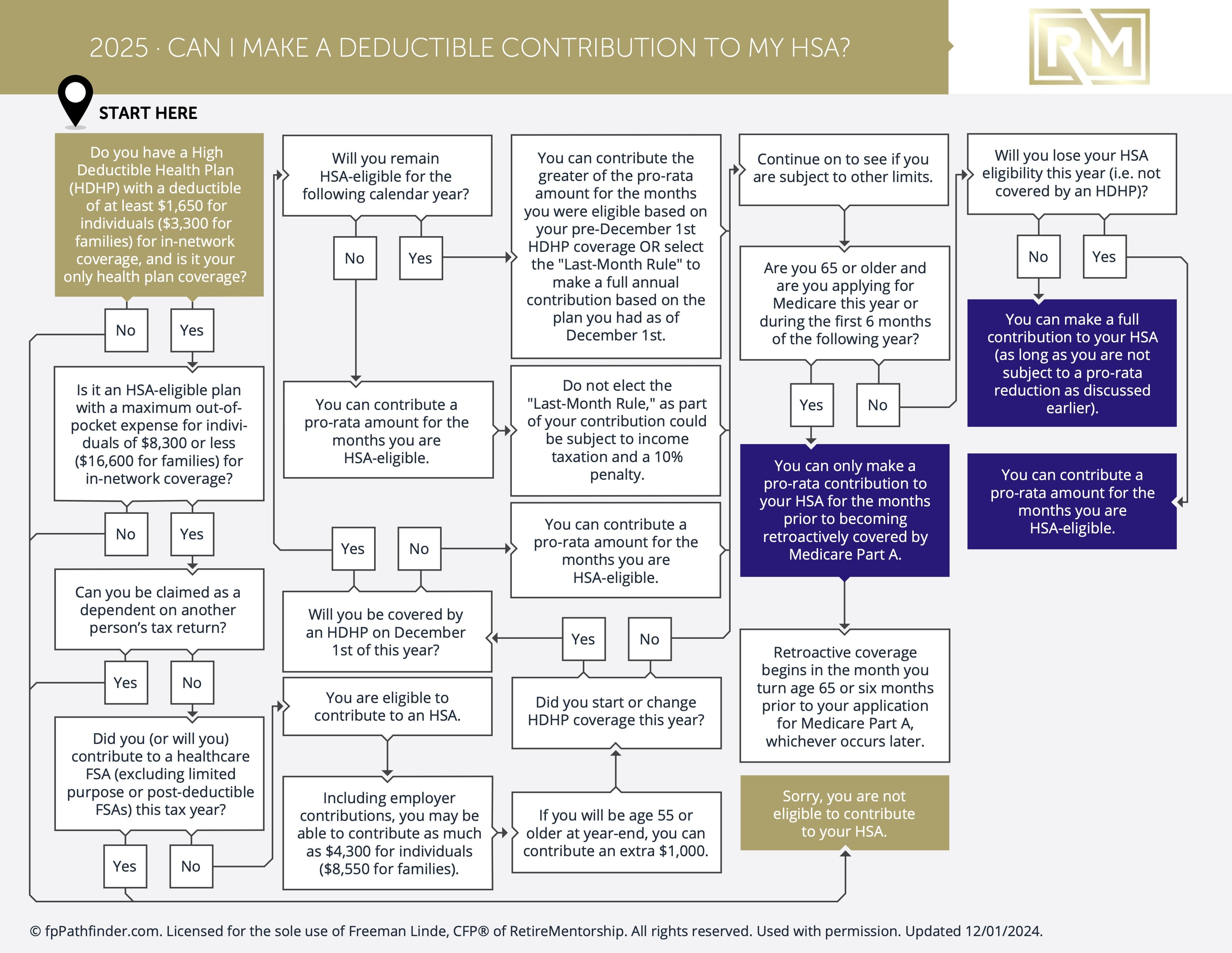

Can I Make A Deductible Contribution To My HSA? This flowchart will walk you through discovering your eligibility.

Title: Maximizing Your Health Savings: Understanding Deductible Contributions to Your HSA

Health Savings Accounts (HSAs) have become increasingly popular for managing healthcare expenses while enjoying tax benefits. One common inquiry among individuals considering HSAs revolves around the feasibility of making deductible contributions. Let’s delve into this topic to grasp the rules, advantages, and considerations associated with deductible contributions to your HSA.

Understanding Health Savings Accounts (HSAs)

HSAs are tax-advantaged accounts tailored to help individuals save for qualified medical expenses. They are accessible to those covered by high-deductible health plans (HDHPs). Contributions to an HSA can be made by both employers and employees, with the IRS imposing certain limits.

Eligibility

To qualify for deductible contributions to your HSA, you must meet specific eligibility criteria:

- Enrollment in an HDHP: Individuals must be covered by a high-deductible health plan (HDHP) to be eligible for an HSA. HDHPs usually entail higher deductibles and lower premiums compared to traditional health plans.

- No Medicare Enrollment: Those enrolled in Medicare are ineligible to contribute to an HSA. Hence, individuals aged 65 or older and enrolled in Medicare cannot make deductible contributions to their HSAs.

- Independent Tax Filing: You cannot be claimed as a dependent on another person’s tax return to make deductible contributions to your HSA.

Benefits

Making deductible contributions to your HSA offers numerous advantages:

- Tax Deduction: Contributions are tax-deductible, allowing you to reduce your taxable income by the contributed amount. This can result in substantial tax savings, particularly for individuals in higher tax brackets.

- Tax-Free Growth: Funds in your HSA can grow tax-free through investments once contributed. This facilitates the accumulation of savings over time, serving as a source of funds for future medical expenses.

- Tax-Free Withdrawals: Withdrawals from your HSA for qualified medical expenses are tax-free. This encompasses expenses such as medical appointments, prescription medications, and medical procedures.

Considerations Before Making Deductible Contributions

Before proceeding, consider the following:

- Contribution Limits: The IRS sets annual contribution limits for HSAs. For 2022, the limit is $3,650 for individuals with self-only coverage and $7,300 for those with family coverage.

- Contribution Deadlines: Contributions to your HSA must be made by the tax filing deadline, usually April 15 of the following year.

- Coordination with Other Accounts: If you have other accounts like a Flexible Spending Account (FSA) or Health Reimbursement Arrangement (HRA), be mindful of coordination rules to prevent potential tax implications.

In conclusion, making deductible contributions to your HSA can offer valuable tax benefits and assist in saving for future medical expenses. By comprehending the eligibility criteria, benefits, and considerations associated with deductible contributions, you can make informed decisions to optimize your healthcare savings strategy. Remember to seek advice from a financial advisor or tax professional for personalized guidance tailored to your unique circumstances.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.