Your Financial Identity

Who are you? How would you describe yourself? What is your identity?

Our identity shapes everything we do, whether we know it or not. Each decision we make is aligned with who we are or who we want to be. Identity is at the core of it all.

All of your financial decisions are based on your financial identity. All your financial outcomes spring from your financial identity. You have a financial identity, and it has a more significant effect on your lot in life than any goals you may have or plans you may build.

Over the next few weeks, we will explore how to change our financial behaviors. Today, we will start at the beginning by exploring our financial identity. I want to flush out a concept introduced to me in the book Atomic Habits by James Clear.

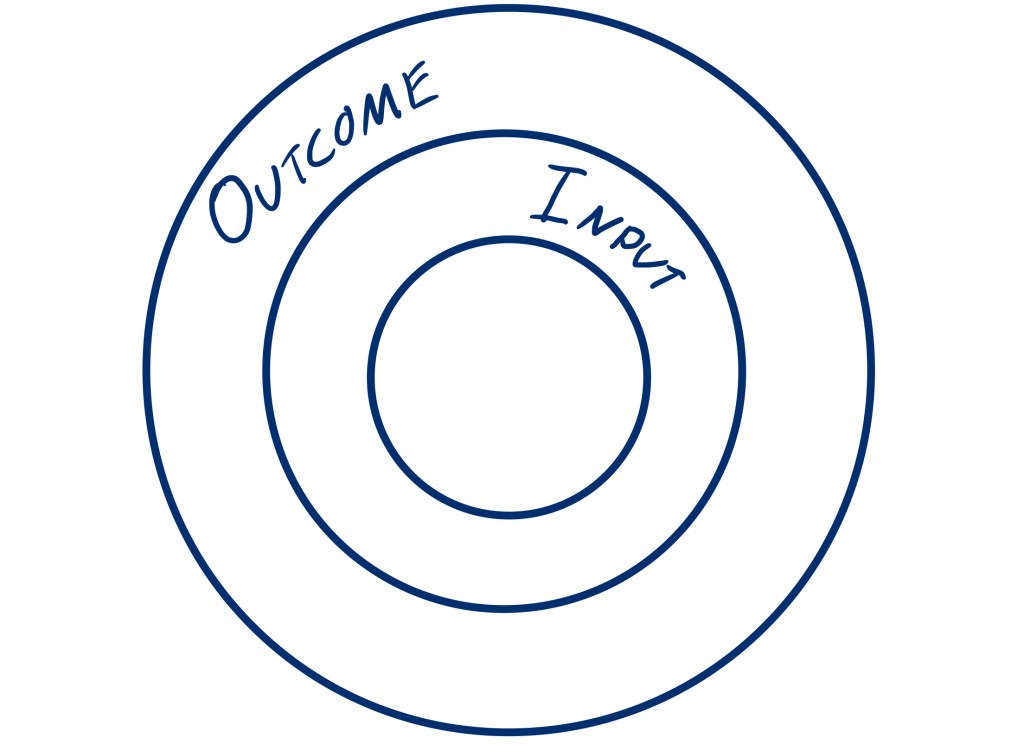

If you want better finances, there are three layers you could focus on.

Outer Layer: Outcome

Outcomes are what we strive for. Almost all goals that are set, financial or otherwise, are outcome-based goals.

Consider these common goals:

What do these have in common? They are outcomes. The result of something else.

Goals are great. I love goals. I’m an avid goal-setter (and somewhat less avid goal-achiever). I love quotes like, “If you aim at nothing, you’ll hit it every time,” and goal-setting tools like the SMARTER Goals framework. I have goals, targets, and plans for every domain of life.

But goals are not enough. Merely having the goal to retire by age 62 won’t enable you to achieve that outcome. That’s when we need to look inward.

Inner Layer: Input

Your input determines your outcome.

It’s good to have a desired outcome. You don’t want to put all your time, energy, and money toward something only to end up with the wrong result. You don’t want to climb a ladder only to find it’s leaning against the wrong wall. Begin with the end in mind.

But then it is all about input. How much do you put in your 401(k) each paycheck? How much do you put in your Roth IRA each month? What time, effort, and competence do you put in to tax planning and reducing your lifetime taxes? (Or how much are you paying a professional to do it for you?)

Input is the plans, tactics, systems, and actions you take to make the outcome a reality, or at least more likely. We need to have an outcome in mind, but after our desired outcome is in mind, we need to focus more on the inputs. James Clear writes, “We do not rise to the level of our goals; we fall to the level of our systems.”

But there is a deeper layer that is even more critical.

The Core: Identity

Who we believe that we are is at the core of all of our actions. If you want different results, you must act differently. And if you want to consistently act in a different way, you must change your identity to support these actions.

Consider the act of smoking. Most people who smoke call themselves “smokers.” Whether it was something they identified themselves or a label that others used that they internalized, people who smoke (action) are called smokers (identity).

Now consider two people trying to quit smoking. Someone approaches and offers them both a cigarette.

The first one says, “No thanks, I’m trying to quit.”

But the second says, “No thanks, I’m not a smoker.”

Who do you think will be more successful at no longer smoking? The guy who identifies as a smoker who is trying to act in opposition to his identity? Or the one who identifies as that which he wants to become?

How you identify with your money shapes the way you act with it and thus determines the results you will achieve, good or bad.

If you are fond of saying, “I’m so bad with money!” you are identifying yourself as someone who is bad with money. You will then proceed to be bad with money. It doesn’t surprise you when you neglect savings, spend more, and go further into debt. Why? Because that’s what people who are bad with money do. And you’re bad with money. If so facto.

Ditto for “I’m so bad at saving money” or “I’m going to have to work until I’m eighty.”

You will live congruently with your identity, whatever that identity is.

Changing Your Identity

But what if you decided to change your identity?

What if you started saying, “I’m responsible with money.” “I make wise choices with money.” “I am a diligent saver.”

You can try and start with the outside and work in. You can begin with the end in mind and work backward to what you need to do to get there. “I want to retire at age 62. Therefore I must save 15% into my 401(k).” It’s unlikely you will suddenly go from contributing 3% to 15%.

Or you can start from the inside out. “I am a diligent saver.” What do diligent savers do? They pay themselves first. They don’t fritter away money on every whim or advertised trinket. “Diligent savers put 15% into their 401(k). I am a diligent saver. Therefore, I put 15% into my 401(k).”

There are no results without action. There are no outcomes without inputs. But what is more likely to change your actions? An external goal dangling out in the future? Or an internal identity driving you from your core.

Related Identities

There is more to your financial identity than explicit “I am bad with money” or “I am a diligent saver.”

Suppose a significant part of your identity is that of a hunter. “I’m a hunter.” What do avid hunters do? They buy guns. Lots of guns. They buy ammo. Hunters buy deer tags, dog whistles, and duck blinds. They buy hunting land, hunting cabins, and hunting trucks. More gear. More guns. Double all of it if they are also “a fisherman.” Why do they spend so much money on hunting and fishing? Because they are hunters/fishermen. And that’s what hunters do. All the hunting magazines, websites, and YouTube channels tell them to do that. They act according to their identity.

Or suppose you are a “shopper.” You “love shopping” and spend thousands of dollars per year “shopping.” You don’t spend the money to invest in a few quality items to enrich your life and the lives of those around you. No one uses most of the items you’ve bought. They’re buried in the closet or the garage or, God forbid, in your storage unit because you ran out of room in your closet and garage. You spend the money because shopping is the experience. It’s a journey, not a destination. And that’s what shoppers do.

Or, you are a “successful business executive.” Therefore you buy high-end suits, gold watches, and luxury vehicles. Why? Because that’s what successful business executives do.

Stronger Together

These identities are maximized when you do them with like people who share the same identity. You hunt with your buddies, and you’re always showing each other the latest in your arsenal. Or you shop with your girlfriends, and you’re always in the latest styles. Or suppose you work and consort with other successful business executives, and you drive what they drive and wear what they wear.

There is nothing wrong with hunting, shopping, or working in business. But when actions morph from something you do to someone you are, they have an enormous impact on your behaviors.

Your other identities shape your financial identity. Some identities cost a lot of money by default. Being “fashionable” means you must have the latest fashions (which change what… hourly?) If you’re a “techie,” you always have the latest smartphone, smart watch, smart TV, smart thermostat, smart vacuum, smart dog, and smart everything else. Being a car guy basically guarantees you’ll be poor because cars are so expensive!

If these identities are stronger than your “diligent saver” identity, you will continue to spend money on your identities instead of saving money for your identity.

Vote for a New Identity

Instead of trying to force yourself to act contrary to your identity, change your identity, or change the priorities or your identities, and then act according to the ideal identity you want.

“I am a diligent saver. Therefore, I will increase my 401(k) savings by 1%, because that’s what a saver would do.” Then you do it.

When you act according to your aspired identity, you are, “casting votes for that new identity.1” When you see yourself acting according to this identity, it reinforces the identity. Confirming your identity encourages you to continue to act out that identity, and it becomes a Victorious Cycle™.

Of course, the opposite is also true. If you believe you are bad with money, you will continue to save less into retirement, spend more on your credit card, and buy items you can’t afford, and these bad behaviors will cast votes for the identity of “someone who is bad with money.”

You don’t have to be perfect. The identity with the most votes wins. Choose the identity you want most, and cast a majority of your votes for that identity.

Final Examples

Instead of “hunter” as your primary identity, perhaps you desire to be a “wise and caring dad, who hunts sometimes.” What would a wise person do? Would a caring person do this or that? What would a good dad do? Hunt during hunting season, but cast more votes for those identities during the rest of the year.

Instead of “shopper” as a primary identity, you simply choose to be a minimalist. You see the heaps of old purchases all around and calculate how much money you have spent on items you never use, and decide to change. Now that you are a minimalist, what do minimalists do? They read or listen to books on minimalism and listen to podcasts on the topic. Minimalists downsize the junk. They are intentional about their purchases. They have other hobbies and experiences other than shopping for shopping’s sake. And they save boat-loads of money in the process.

Conclusion

What do you want as outcomes? Who is the type of person most likely to achieve those outcomes? What current identities conflict with that desired identity?

You can choose, today, to be someone new. Act according to that identity—cast votes for that identity—and it will become your true identity. Behavior change, with finances or anything else, takes place at many levels. But it begins at the core of who you are: your identity.

1. Concept by James Clear in Atomic Habits.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.