How Are Financial Habits Made?

Financial habits rule our financial results. “We are what we repeatedly do. Excellence, then, is not an act but a habit.”

No one sets out to fail with finances. No one desires to be mediocre with money. We want to be successful with our salary, capable with our capital, adroit with our assets, and wise with our wealth. We seek excellence.

Excellence with personal finance comes from good financial habits. A single act of contributing to a Roth IRA does not make you wealthy. But a habit of saving will change your life.

Charles Duhig explored the Power of Habit in his seminal book. Many things we do in life are based on habits, not conscious choices. James Clear further expanded on this work with his must-read book Atomic Habits. Both are worth reading, but Atomic Habits is in my top ten, and possibly my top five list of books everyone should read.

We’ll look at how habits form today, and over the next two weeks, we’ll cover how to build good ones and break bad ones.

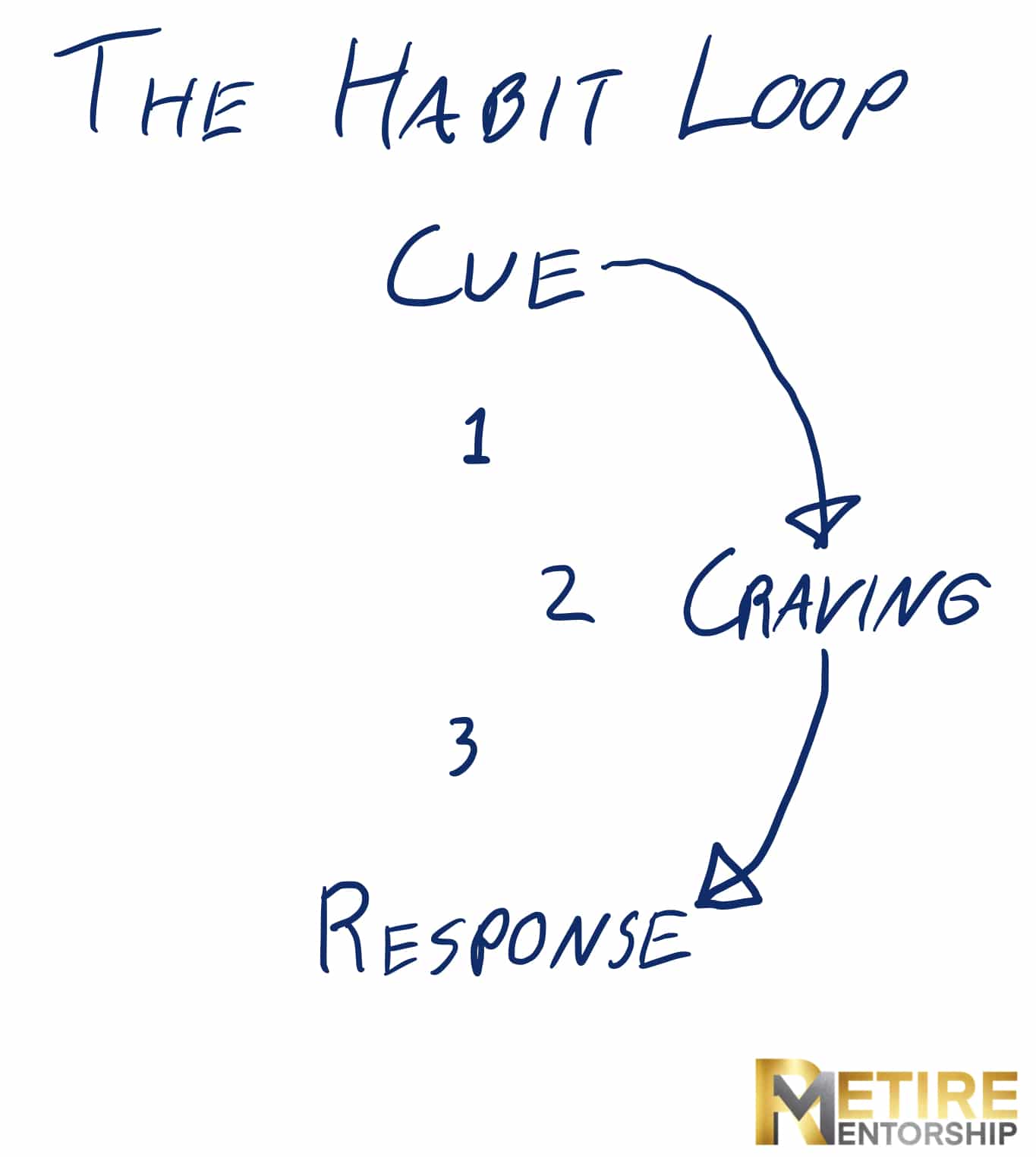

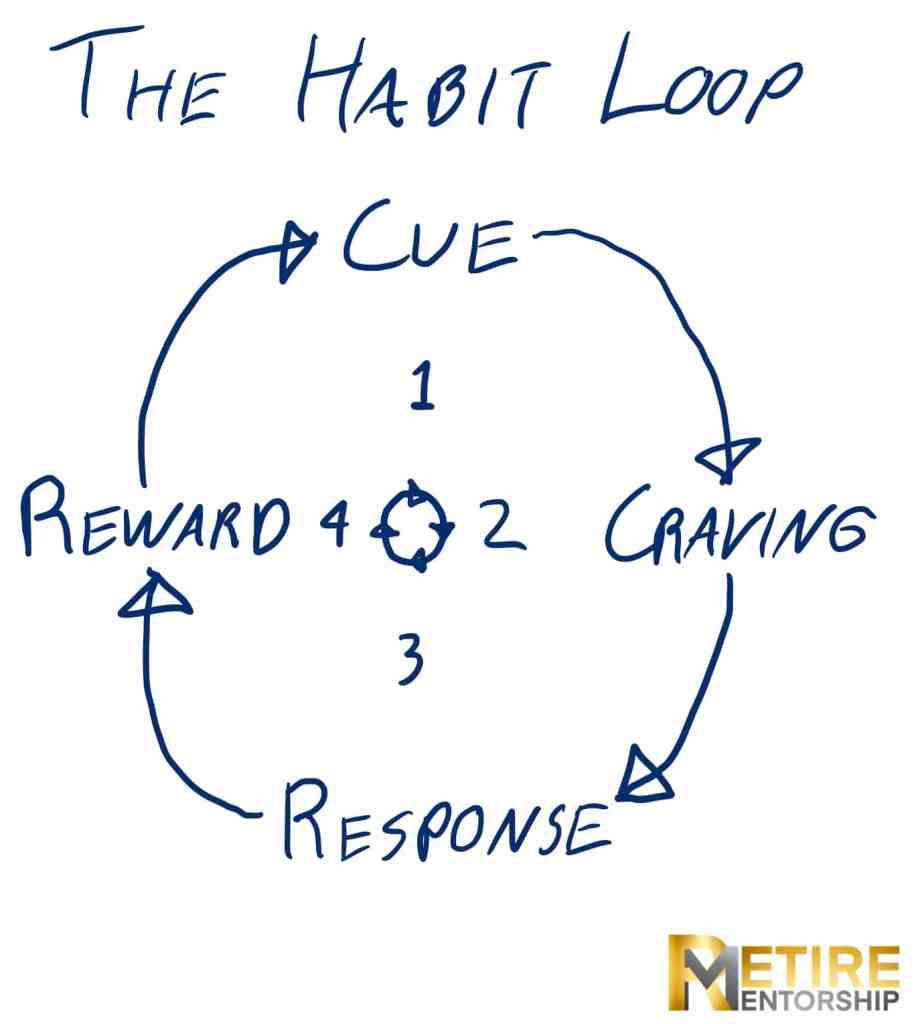

Habits are made following a concept called the Habit Loop.

The Financial Habit Loop

Every habit we have, good or bad, financial or otherwise, is created using the Habit Loop. There are four phases of the loop, and we’ll look at each.

We will also explore a financial habit along the way, the habit of the DSD.

Financial Habit: The Daily Starbucks Drink

Many folks have this habit or something like it that has massive financial ramifications. Consider those who make a stop every day at [insert coffeehouse of choice, we’ll use Starbucks for the rest of the episode]. If you go to Starbucks Monday through Friday and spend $5 on average, that’s $25 per week, $100+ per month. One could brew a drink from home for $0.50. That would equate to $10 per month. This habit is costing you $1,000 more per year than brewing from home. ($90 more per month, times 12 months, is $1,080.)

Is a Daily Starbucks Drink a Bad Habit?

Attorney answer in 3… 2… 1…

“That depends.”

If you have completed your financial plan and are monitoring it, then you can know if the DSD is a bad habit or not. If you have not completed a financial plan, you will not be able to answer that question. Let’s assume you have completed one since we can’t answer unanswerable questions.

Let’s say you have completed your plan and you are saving as much as you should toward retirement in your 401(k)s, Roth IRAs, HSAs, and other accounts. You are on track to retire on your terms. Or you have already retired and your plan calculates you can spend $X per year, and your coffee habit falls inside that $X per month. Your retirement can support your venti, extra hot, double cup, triple-shot, oat milk, no whip, extra crema, french vanilla latte habit.

If you are on track to meet your financial goals as evidenced by your financial plan, then a Daily Starbucks Drink is not a bad financial habit. It may be a bad health habit, but that’s beyond the scope of this episode.

But if you are on track to run out of money in retirement or you are not on track to retiring because you are spending too much, then spending $1,000 per year on Starbucks is probably a bad financial habit.

Turning a Bad Financial Habit into a Good Financial Habit

What if you turned that DSD into an MRC, a Monthly Roth Contribution? That $100 per month saved into a Roth IRA invested in equities averaging 10% over thirty years comes out to over $225,000 more in your retirement. Tax-Free! Or if you’re already retired, it’s $225,000 more in your retirement at the end of it to pass on to your children and grandchildren, churches, and charities. Or to ensure you’re not a burden on them if you’re in danger of running out.

Tiny habits have big results. Five bucks at Starbucks doesn’t seem like much on a daily basis. But when compounded over thirty years, it has a massive impact. Time magnifies the margin between success and failure.

So what are the components of the Habit Loop, and how do those contribute to our Daily Starbucks Drink habit and all our financial habits?

The Habit Loop Phase 1:

The Cue

The beginning of making a habit is the Cue. You see, smell, hear, feel, or otherwise experience something that sets off a chain reaction.

You’re driving to work in the morning and you see the Starbucks on your usual route. The cue is seeing the coffeehouse.

Most cues for our habits are visual. A disproportionate amount of our brain is dedicated to sight, and it can cue up all kinds of habits. In this case, merely seeing a Starbucks fires up the Habit Loop and in a fraction of a second you move to the next phase.

The Habit Loop Phase 2:

The Craving

Seeing Starbucks triggers the Craving. Now you want your special drink. You remember the sweet french vanilla taste over a smooth oat milk body with rich crema. You remember the boost in focus and alertness from the triple-shot. It’s just the thing you need to transform this dreary Monday morning commute into “an experience.” Thus the craving for your favorite drink leads to a decision in phase three.

The Habit Loop Phase 3:

The Response

Seeking to satiate your craving, you pull into the Starbucks drive-through. Your response is to “cave to the crave.” Because after all, you deserve it.

Note that the response is not the ordering of the drink at the microphone. It is turning into Starbucks. We face cues and cravings all day every day. But our response is what shapes our lives. When we respond in the affirmative to bad habits, or negatively respond to good ones, we start to build the bad and break the good habits in our lives. Especially when that response ends with the last phase.

The Habit Loop Phase 4:

The Reward

You get your fancy drink, take that first sip, and you experience that bliss. Your dopamine receptors go off and you fully enjoy every second of it. Thus your dreary drive turns into an excellent experience.

As a result, your brain now records that sequence.

If I see A, I will want B. And if I respond with X, I will get Y, which is very rewarding! Therefore, every time I see A, I will follow the steps to get Y. Automatically.

The Financial Habit Loop

Tuesday rolls around and you’re driving off to work.

Cue: You see Starbucks on your regular commute.

Craving: You desire your froofroo latte. It tasted so good yesterday! And you swear you were more focused all day.

Response: You pull into the drive-through. Might as well enjoy this commute as well.

Reward: You’re sippin’ sweet once again, and fully enjoying it.

This one act goes around the financial habit loop again, and again, and again. Rinse and Repeat. Habit.

Goodbye $225,000, tax-free. We gave that to Starbucks. I’m pretty sure they need it more than we do anyway.

Conclusion

In conclusion, all good and bad financial habits are built this way. Cue, Craving, Response, Reward.

Now that we know this, how can we use this knowledge to build good financial habits and break bad ones? We’ll discover that next week.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.