When Should I Change My Investments?

When should I change my investments? Generally, I get that question in response to some external stimulus.

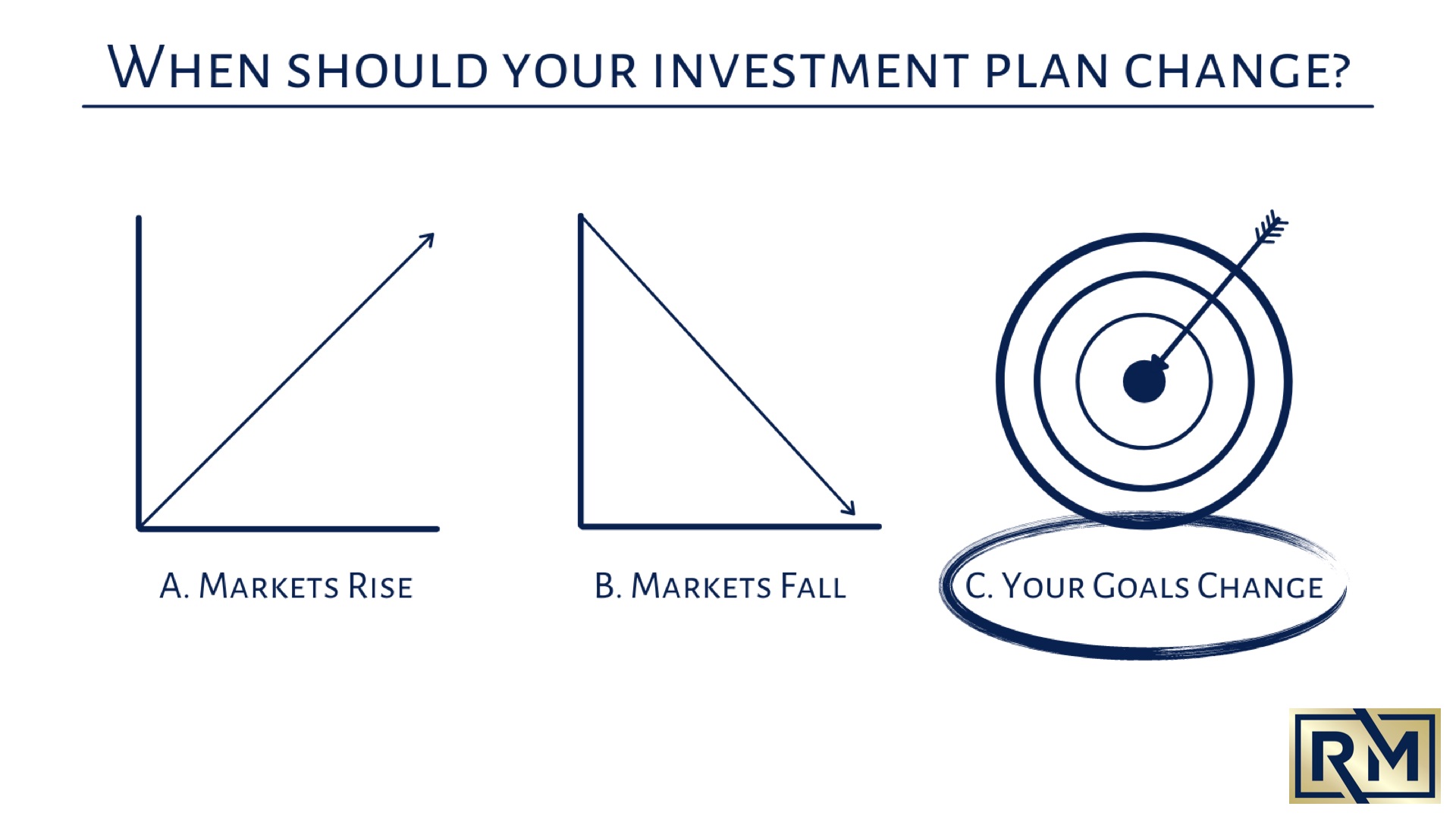

Should External Stimulus Change My Investments?

Sometimes that stimulus is negative. There is a Global Crisis of some kind. The market is in free fall. The talking heads are prognosticating the end of the world. Is now the time to change?

Sometimes the stimulus is positive. New economic data looks good. The markets are surging! Perhaps we’re entering the Roaring 20s, the 2020s, not the 1920s. Do we need to make some adjustments to take advantage?

Sometimes that stimulus is neither. Your brother-in-law was discussing some new investing ideas. You got an email about an opportunity. Someone at the Y was boasting about their investment returns, which seemed better than yours. Are we missing out?

The Reason We Invest

Before we change our investments, we must remember why we have what we have now. And to remember that, we must revisit the reason we invest in the first place. Let’s go back to the beginning.

It starts with a Goal. What are you trying to accomplish? What do you want your money to do for you? Are you saving for retirement? Will you be using that money for retirement income? Are you saving for a down payment on a house or a cabin? What is the goal for your money?

After you clearly have a goal, then you create aPlan. What will give you the best chance of achieving that goal? Your plan is then funded by a Portfolio.

Inside that portfolio, you will decide your Asset Allocation, the percentage of your money devoted to ownership of the best businesses in the world, and the percentage you are lending to those companies and governments. You must also decide your Diversification, the types of businesses you will own or lend to, and the Fees you want to pay. Then you’ll Select Your Investments.

We covered this in Episode 111, Investing Order of Operations. Refer to that episode for more details.

Thus, the reason we have what we have now is because they are best suited to achieving our goals. Your investments shouldn’t change unless your goals have changed.

Should I Change My Investment if My Goals Change?

Now, maybe your goals have changed. This can take a lot of forms.

Perhaps you thought you would live in your current home for decades, so all your investments are geared toward the long term. Then your life changes, and you need to buy a new home which will require a sizeable down payment in the next 3-6 months. You will need to change your investments since your timeline changed.

Perhaps you’ve been planning to retire in two years for a while now. But you just switched careers and now can’t imagine retiring. Again, your goals have changed, so your investments will likely change too.

If your goals change, then your investments may change too. Your investments are the funding mechanism for your goals. We begin with the end in mind. Thus, when the end changes, the beginning may change too.

I say “may” change because it’s not a certainty. If your goal changes from retiring in 15 years to retiring in 10 years, your investments likely don’t need to change right now. But the point at which you would change your investment from pure accumulation to income will be much sooner.

Reactive vs. Proactive

Ultimately, we’re talking about the difference between being proactive and reactive.

Reactive investors are constantly watching the news and hunting for tips, tricks, and changes in the wind. They react to breaking news, shifts in polling data, and new economic forecasts.

(Here, we must remind ourselves of the quote by Nobel Laureate Economist Kenneth Galbraith, “Economic forecasting exists to make astrology look respectable.”)

Investing is not tennis. We are not constantly poised on the balls of our feet, muscles tense and heart racing, as we wait for our opponent’s serve to determine which way we will move. What an exhausting and fruitless strategy.

Good investing is much more like watching grass grow. If you want excitement, go to the casino.

We don’t react to what is happening in the external world. We make a plan and proactively save and invest toward that plan.

It’s a much better and more peaceful approach.

When should you change your investments? When your goals change.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.