Fixed Income = Fixed Losses

When the “stock market” gets scary, folks flee to the “safety” of fixed income. But is there any real safety there? Or does switching to fixed income = fixed losses?

Fixed Income Isn’t Safe

The most common reason people don’t invest in equities is because they are “risky.” You could lose your money. So they invest some of their money in fixed-income investments (such as bonds, CDs, annuities, government securities, and the like). They believe these investments are “safe.”

But Fixed Income is not safe. Here are two reasons.

Fixed Income is Not Immune to Volatility

The value of most fixed-income securities is subject to volatility, just like equities. It’s supposed to be less volatile. But 2022 taught us an important lesson: Fixed-income investments can lose big time. Here are the approximate losses we saw from their peaks to their lows across corporate bonds in the last few years.

- Short-Term Bonds: -7.7%

- Intermediate-Term Bonds: -17%

- Long-Term Bonds: -39%

Some of their value as recovered. And their interest payments mean that their total return is not that bad. But the lived experience of losing that value is still real. Are bonds really that safe?

Fixed Income Gets Crushed By Inflation

Bonds are a terrible hedge against inflation. According to the Quantitative Analysis of Investor Behavior (QAIB), the main bond index has averaged 3.17% over the last twenty years. Inflation of that time has averaged 2.59%. The real after-inflation growth has been less than a percent.

Is that safe? To have money that’s not growing? If you are in retirement and have a 4-5% distribution rate, how is your money that is making you less than 1% going to sustain that?

Fixed Income Loses to Perfect Timing

Okay, so fixed income as a long-term growth strategy is not a good strategy. But what if you pair it with equity investing and a bit of good timing? A common strategy people try is to time the market. Stay invested in equities, but try to pull out before a market crash.

Suppose you timed 2020 perfectly. You pulled out on January 1 based on whispers of a contagious coronavirus. You were right. The equity markets plummeted. You were safe and sound in Vanguard’s Total Bond Fund. You didn’t quite believe the recovery was real, and there was an election coming, so you stayed in bonds. Then, you were justified again when the equities plummeted in 2022. Everything seemed to be going well. You were safe and sound in your bonds while the stock market was in freefall. Then your bonds began to fall too.

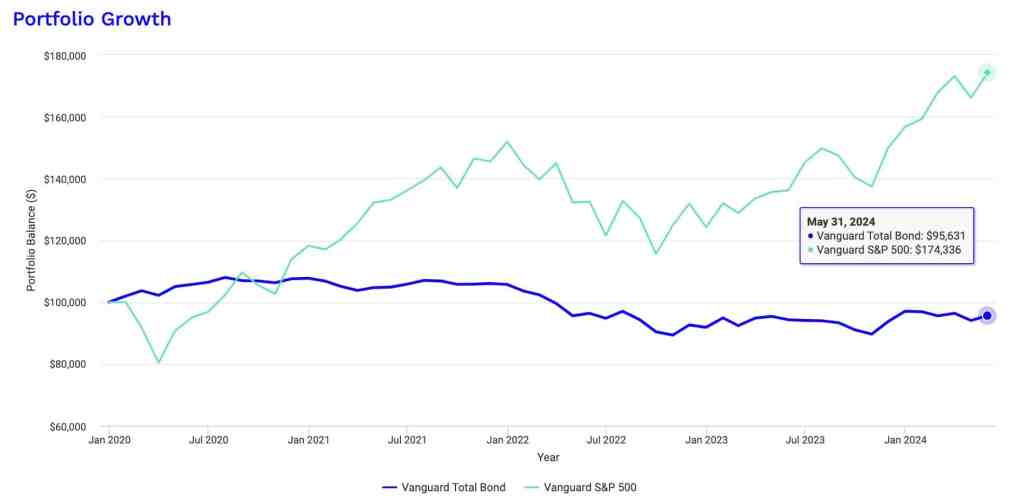

Even if you had perfectly pulled out before the last two bear markets, you were not better off. Here are your results in real Vanguard funds over that time.

$100,000 invested from January 1, 2020, through May 31, 2024, would be worth:

- $95,631 in the Vanguard Total Bond Fund

- $175,336 in the Vanguard S&P 500 Fund.

You lost money in “safe” fixed income and nearly doubled your money in “risky” equities, even through two bear markets in four and a half years.

“I didn’t do that,” you may be saying. “I know not to time the market.”

But was 40% of your allocation already in bonds? Did you have a balanced 60/40 portfolio? Was your money (or part of it) in a target date fund? It makes no difference if you moved to bonds in 2020 or were already there. You’ve lost money since 2020 in “safe” investments.

Fixed Income Compounds Investors’ Bad Behavior

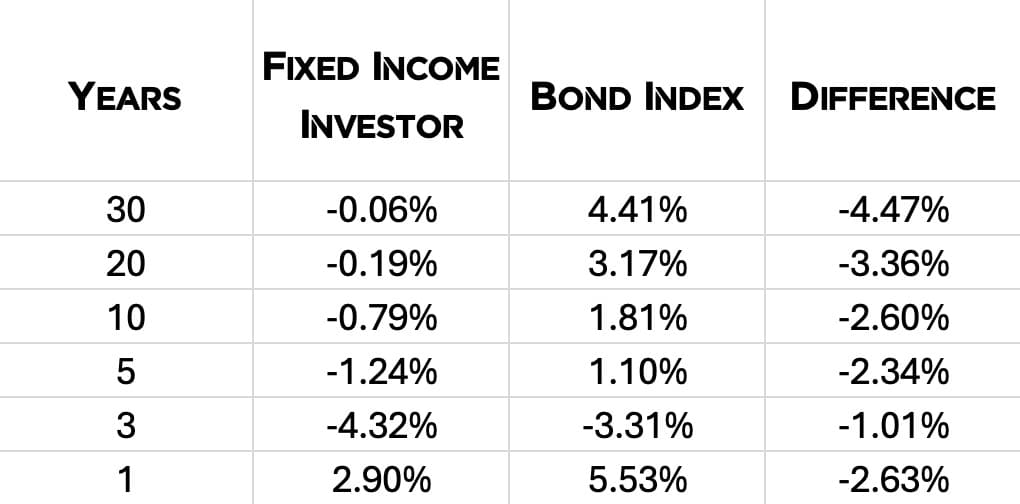

The Quantitative Analysis of Investor Behavior paints an even worse picture. As we know, there is a difference between investment returns (which is what we’ve discussed so far) and investor returns. The effect of investor behavior on equities is stark. And it is no better for fixed income. Behold, the returns of the Average Fixed-Income Investor:

Fixed Income: A Fixable Problem

Fixed income is a fixable problem.

I don’t know what equity sector is going to outperform over the next 3-10 years. No one does. But we can be supremely confident that equities will vastly outperform fixed income over that time.

My main goal is to help investors reduce their fixed-income exposure and increase their ownership in the best businesses in the world. Becoming a business owner (equity investor), and staying one through thick and thin is the best way to increase your returns. Let’s focus on what we can control: our asset allocation and our behavior.

Again?

You may be thinking, “Haven’t I heard this before? Why are you saying the same things over and over again.” We need to be reminded more often than we need to be taught. If necessity is the mother of invention, then recessity is the mother of retention. Reciting the same truths over and over again is what gets them to stick—what causes us to believe. And we don’t act on what we know. We act on what we believe. That’s what we’re here for.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.