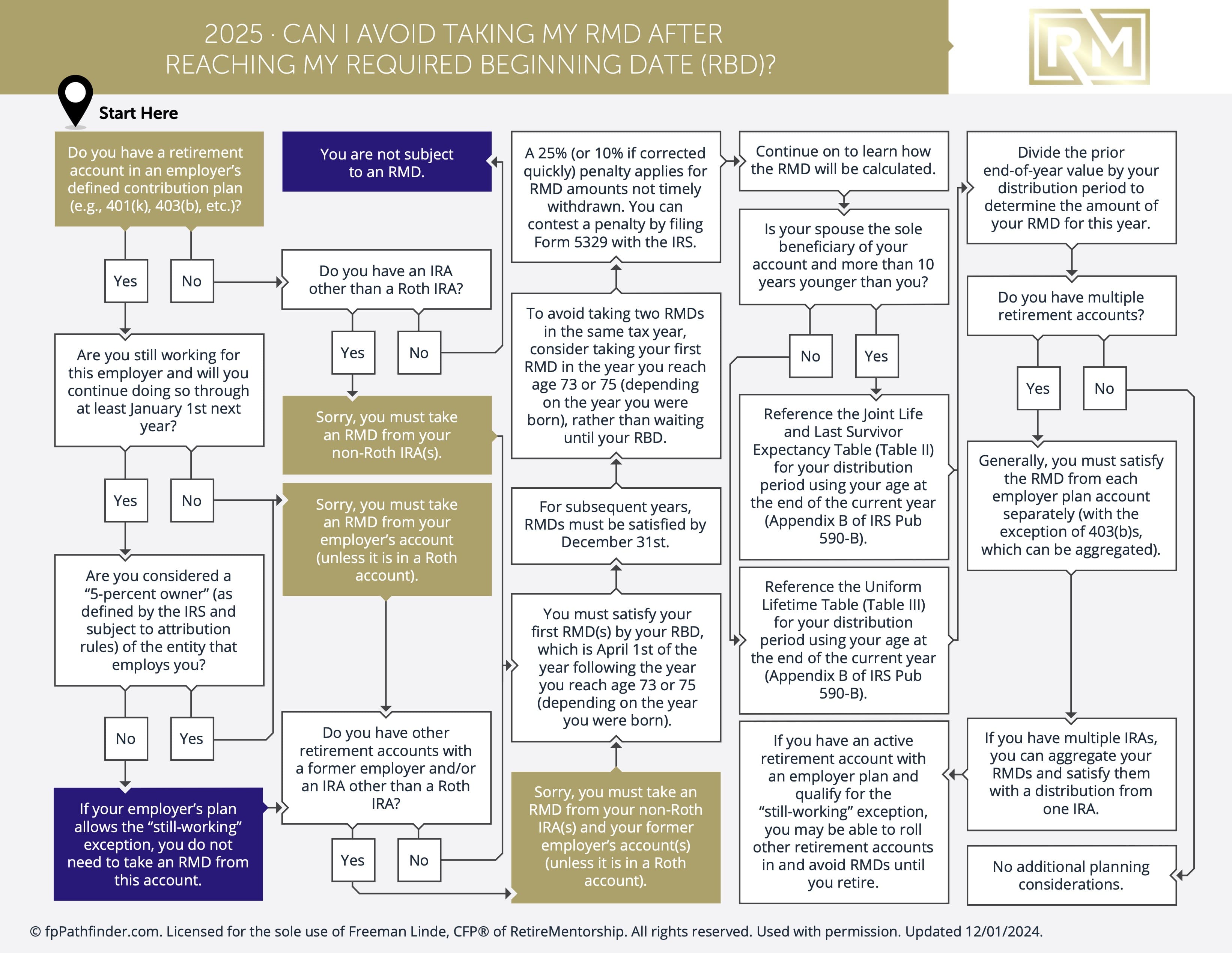

Can I Avoid Taking My RMD After Reaching My Required Beginning Date RBD?

Can I Avoid Taking My RMD After Reaching My Required Beginning Date RBD? This flowchart will walk you through discovering your eligibility.

Introduction: Deciphering RMDs and the RBD

Navigating Required Minimum Distributions (RMDs) after reaching the Required Beginning Date (RBD) can be a daunting task in retirement planning. Understanding the nuances of RMDs and exploring potential strategies to avoid them becomes essential as you approach this significant milestone.

1. Understanding RMDs and the RBD

RMDs represent the minimum withdrawals you must take annually from retirement accounts once you reach a certain age. The RBD, typically falling on April 1 following the year you turn 72, marks the deadline for taking your initial RMD.

2. Exploring Options to Dodge RMDs Post-RBD

While the RBD signifies the beginning of RMD obligations, certain scenarios may offer opportunities to circumvent them:

3. Extended Employment Beyond the RBD

Continuing to work beyond age 72, if allowed by your employer’s retirement plan, could delay RMDs from that specific plan until retirement. However, this exemption applies only to the employer’s plan you’re actively participating in, not other accounts like IRAs.

4. Harnessing Roth IRAs and RMDs

Roth IRAs exempt holders from RMDs during their lifetimes. If you’ve converted traditional accounts to Roth IRAs or have Roth contributions, you’re exempt from RMDs. Strategic utilization of Roth accounts provides flexibility in retirement income and tax planning.

5. Maximizing Qualified Charitable Distributions (QCDs)

Individuals aged 70½ or older can execute Qualified Charitable Distributions (QCDs) directly from IRAs to qualified charities. QCDs fulfill RMD requirements while excluding distributed sums from taxable income. This dual-purpose approach benefits retirement savings and charitable causes alike.

6. Keeping Pace with RMD Regulations

RMD rules are subject to change, emphasizing the importance of staying updated on any revisions or adjustments. Collaborating with financial advisors or tax professionals can help navigate evolving regulations and optimize retirement income strategies accordingly.

Conclusion: Strategic Retirement Planning

Effectively managing RMDs post-Required Beginning Date demands strategic retirement planning and a deep understanding of applicable rules and exceptions. By exploring tactics such as extended employment, leveraging Roth IRAs, and utilizing Qualified Charitable Distributions, you can potentially mitigate RMD obligations and refine your retirement income strategy. Stay vigilant, regularly review your retirement plan, and seek guidance from financial experts to maximize your retirement savings while adhering to RMD mandates.

Can I Avoid Taking My RMD After Reaching My Required Beginning Date RBD?

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.