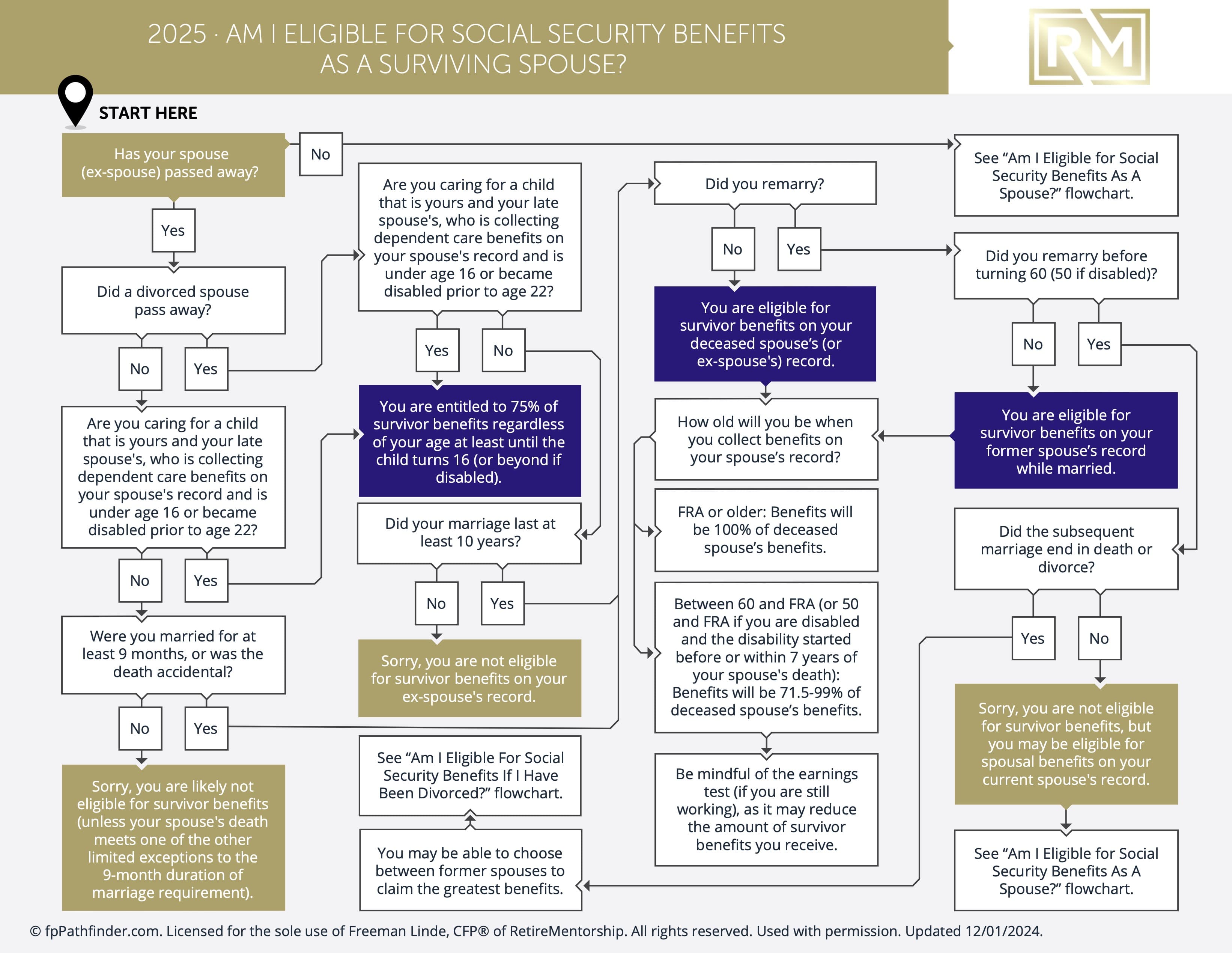

Am I Eligible For Social Security Benefits As A Surviving Spouse?

Am I Eligible For Social Security Benefits As A Surviving Spouse? This flowchart will guide you through the factors determining eligibility.

For surviving spouses grappling with financial concerns following the loss of their partner, understanding eligibility for Social Security benefits can provide much-needed relief. Are you wondering if you qualify for Social Security benefits as a surviving spouse? In this comprehensive guide, we’ll navigate through the eligibility criteria, benefits available, and steps to ascertain your entitlements in detail.

Eligibility for Social Security Benefits as a Surviving Spouse

Eligibility for Social Security benefits as a surviving spouse hinges on several factors. These factors include age, relationship to the deceased, and work history. Here’s what you need to know to determine your eligibility:

- Age Requirement: Surviving spouses must be at least 60 years old (or 50 if disabled) to qualify for Social Security survivor benefits.

- Relationship to the Deceased: You must have been married to the deceased for a minimum of nine months to be eligible for survivor benefits. Exceptions may apply in cases of death resulting from accidents or while in the line of duty.

- Benefits Based on Deceased Spouse’s Work History: As a surviving spouse, you may be entitled to benefits based on your deceased spouse’s earnings record. This provides crucial financial support during retirement.

- Own Work History: If you have your own work history and qualify for Social Security benefits based on your earnings, you may have the option to choose between benefits based on your own record or those of your deceased spouse, depending on which yields a higher benefit.

Maximizing Social Security Benefits as a Surviving Spouse

To optimize your Social Security benefits as a surviving spouse, consider implementing the following strategies:

- Delaying Benefits: Postponing Social Security benefits can result in higher monthly payments. If feasible, consider delaying benefits until reaching full retirement age or beyond. (currently 66 to 67, depending on your birth year)

- Claiming Strategies: Explore various claiming strategies to maximize your benefits. Such as filing a restricted application for spousal benefits while allowing your own benefits to accrue, or vice versa.

- Consultation with a Financial Advisor: Seeking guidance from a financial advisor or retirement planner can help you navigate the complexities of Social Security rules and claiming strategies, ensuring you make informed decisions regarding benefit claims.

Conclusion

Navigating Social Security benefits as a surviving spouse can be daunting, but understanding the eligibility criteria and available benefits is essential for securing your financial future. By familiarizing yourself with the eligibility requirements, exploring claiming strategies, and seeking professional advice, you can optimize your Social Security benefits and alleviate financial concerns during retirement. Take the first step towards securing your financial well-being today by exploring your eligibility for Social Security survivor benefits.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.