Creating a Financial Plan 6 – In-Retirement Planning

“The trouble with retirement is that you never get a day off.” ~Abe Lemons

Effective football coaches don’t wait until after kick-off before putting together a game plan. They study the opposing team and their own players for weeks in advance, consult their other coaches, and put together the playbook well before game day.

Likewise, don’t wait to start your In-Retirement Planning until you’re… in retirement. Ideally you should start planning this in earnest ten years out from your target date, and you should have an established plan by five years out. You may have to make adjustments and call some audibles, but the framework should already be there.

In-Retirement Planning encompasses your finances in retirement, specifically Retirement Income, Social Security, and Medicare. The other elements of planning still apply in retirement (taxes, anyone), but this piece shifts from saving for retirement to spending in retirement. Let’s look at each.

Retirement Income

You’ve saved and invested for decades. Now you’ll need to spend it. You’ve always lived on an income and that won’t change simply because you aren’t working. You will need an income in retirement.

Specifically, you need Three Dimensional Retirement Income, income that covers the three D’s.

- Duration – Income that lasts as long as you do.

- Direction – Income that rises faster than the cost of living.

- Deviation – Income that flexes with your variable expenses.

You need a plan for how to create this income. And it must satisfy all three aspects.

Someone might offer you an annuity that “guarantees” to pay you an income for your lifetime. But it’s flat. Sure that income might be able to afford a box of Corn Flakes when it’s $4 each. Cheerios at $4, $6, $8, $11.

Total Return vs Income

30 year returns:

- Equities: 10%.

- Bonds: 6% (about half in the last 10).

- Inflation. 2.4%.

Bonds are2.5x inflation. Equities are 4x inflation. Equities are a better hedge against inflation.

Your retirement will be impacted by Sequence of Return Risk, the order in which your returns come. You need the Red Bucket, Blue Bucket strategy.

At retirement, you need 2-4 years of expenses in cash and bonds (Blue Bucket). The remaining in equities (Red Bucket). Have a plan for when to switch from Red to Blue.

Equities are up 4/5 years on average. Your principal income will come from Red Bucket four out of five years on average. In the other year, you will pull income from Blue Bucket. Restock Blue in from Red Bucket in good years.

Social Security & Pensions

Do not calculate when to take Social Security in a vacuum. It depends on your Investing Plan. There are joint considerations as well. The survivor gets the greater of the two. Do you let one grow to maximize long-term single income? Your timing may depend on the market cycle.

Create a tentative plan and factors that would change it. The same is true for pension timing.

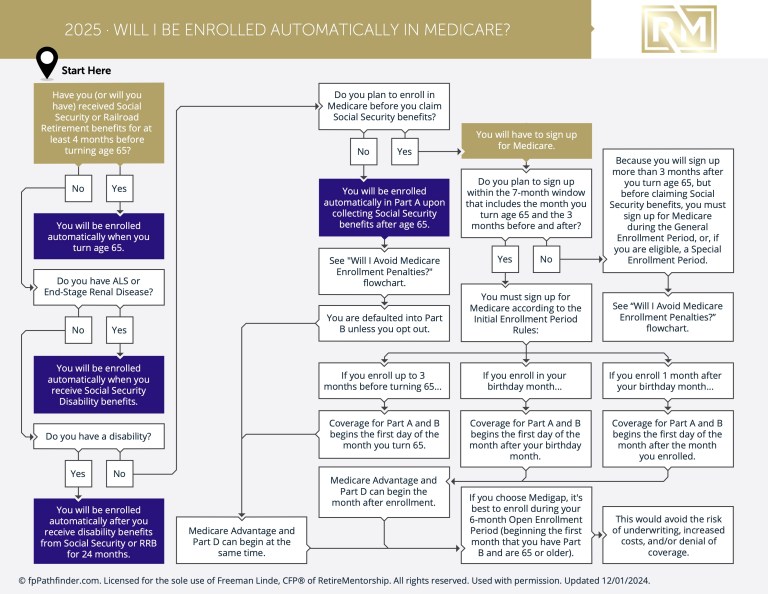

Medicare

You’ll need to plan for Medicare as well. There are four parts to Medicare:

- Part A – Hospitalization – Free

- Part B – Care + Preventative – Flat rate, adjusted annually, + more of higher income.

- Part C – Medicare Advantage

- Part D – Prescription Drugs

There is no max out of pocket on A & B. Consider Part C plan to add MOOP.

Avoid Medicare Supplements. No need to level costs if your retirement income can handle the spikes.

Conclusion

You MUST start your In-Retirement Planning if you are 10 years or less away from retirement.

If this sounds complicated, it is. A good plan will take all the complexity and generate a simple way forward.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.