Belief Over Knowledge

If you don’t stand for something, you will fall for anything. ~Gordon A. Eadie

Welcome to RetireMentorship, Your Mentor to and Through Retirement. I am your host, Freeman Linde, Certified Financial Planner.

It doesn’t matter what you know, only what you believe and do. Let’s talk about why belief is more important than knowledge. First: the Two-Min Tune-In, the primary points of the podcast in the first two minutes.

Point 1: Knowledge is Essential and Insufficient

You can’t do anything without knowing what and how. We do not downplay knowledge. You cannot earn greater investment returns, save on lifetime taxes, protect your family, and ensure it all goes to whom you want it to when you die without knowing how. Knowledge is essential. But knowledge is insufficient. If knowing were enough, we’d all be billionaires with six-pack abs.

Point 2: Action Alone Improves Lives

You can know what to do, but it is useless if you don’t act on that knowledge. You know you need to save for retirement, but nothing changes unless you increase your savings rate. And you know how to attain your ideal health. But if you don’t eat more vegetables, cut down on the sugar, and exercise, the ideal will never happen. You must act.

Point 3: People Act on What They Believe

People don’t act on what they know. They act on what they believe. I know I should order that sun-burst chicken salad, and I know that I would feel better two hours from now if I did. But right now, perhaps only subconsciously, I believe that this half-pound bacon burger and fries will be more satisfying. Until you believe what you know, you won’t act on it.

Point 4: You Can Build Your Belief

There are time-tested strategies for building your belief in what is best for you. Know what to do. Build your belief in that knowledge. Act for the benefit of yourself and your loved ones.

Let’s explore these deeper.

Belief Over Knowledge

You can know what you should do, but you will not act until you believe that you should do it over all other things. That is not to say knowledge isn’t important.

Knowledge is Essential and Insufficient

You must know. But for a few accidents, no one does anything worthwhile without first knowing about it. Knowledge is essential, especially in the complex world of finances.

I’m going to confess a bias of mine. I love knowing and learning. Therefore, I enjoy listening to and reading new material. I consume fifty-two non-fiction books a year and have been adding a professional designation each year as well. I’m dedicated to continual improvement and being the best for the clients of my planning practice.

I say all this not to brag but to demonstrate that I love learning and knowing. Knowing is essential. But an observation I consistently make when I meet with new potential clients of my practice is that people don’t know what they don’t know.

We talked about this a bit in the Introduction to RetireMentorship that financial literacy is in America is terrible. It’s not a required class in most schools or even universities. Most people know what they know about money from their parents or the marketing departments of banks, credit card companies, and insurance companies.

Perhaps they’ve read a book or two or met with a Financial Advisor before. Often they thus think they know what they need to. They don’t realize there is more out there to be understood. Or they don’t know that what they think they know is wrong.

As Mark Twain put it, “It isn’t what you don’t know that kills you. It’s what you think you know for sure, that just ain’t so.”

Perhaps what you think you know leads you down a path of more lifetime taxes, lower lifetime returns, and a reduced chance of achieving what you want.

You can’t change that path unless you know what you should know. You need to know. It is essential. But you certainly don’t need to know everything.

I had a new client once who was very excited about finances. He said to me with gusto, “Teach me everything you know about money!”

To which my reaction was, “No.”

If I taught you everything I know about money, you would know a lot of useless information. You’d have a wealth of conflicting strategies and know more about elements that don’t involve your situation than about elements that do. Knowing everything is a lot of work and mostly useless. Knowing everything is useful for those who play Jeopardy and no one else.

Instead, I’ll teach you what you need to know. I’ll filter out all the false, misleading, and useless information so that you can focus on what is essential. From there, we can formulate a plan and act on that plan. First, though, you need to know. Knowing is essential.

It is also insufficient.

The most obvious proof that knowledge is not enough is the famous “but.”

- “I know, but.”

- “I know… But…”

- “I know I should save for retirement… but I want the 2021 Ford F150.”

- “I know I need to go to the gym… but I was up late last night and slept in instead.”

- “I know I shouldn’t carry a balance on my credit card, but I get a lot of points!”

- “I know… But…”

We know, but we don’t do. Knowledge is insufficient.

We have thousands of self-help and improvement books available to us, and we consume them. I love them. So if there is all this “life-changing,” “optimizing,” “reach your potential” knowledge out there available at only $15-$25 and six hours of reading, why aren’t we all there? Why isn’t everyone self-actualized and living their best life?

The quote bears repeating. “If knowing were enough, we’d all be billionaires with six-pack abs.”

Knowing is essential and insufficient.

What else do we need?

Action Alone Improves Lives

It doesn’t matter what you know; if you don’t act on it, it won’t change anything. Knowing and not doing is the same as not knowing.

If you don’t cut out sugar and vegetable oil, you won’t get healthier. If you don’t have a weekly date night with your spouse, your relationship will suffer. And if you don’t spend time with your kids when they’re kids, don’t be surprised if they don’t want to spend time with you as adults.

It doesn’t matter if you know you should do these things if you don’t do them. Action alone will lead to the outcome you want.

- If you don’t increase your savings rate, you won’t have enough money later.

- If you don’t allocate your investments correctly, they will not outpace your cost of living.

- If you don’t have the right insurances, you will be financially destroyed when something terrible happens.

- If you don’t make the contributions, conversions, and transfers and don’t claim the deductions and credits, you will pay more taxes over your lifetime.

You can read all about finances, but it’s useless if you don’t do any of it.

This point is so obvious; I don’t need to say anything else about it. But I will ask: If action is so necessary, why do so few follow through?

Lack of knowledge? Sometimes. Lack of discipline? Yeah, probably. Because life gets in the way? A ubiquitous excuse, and only an excuse.

I believe that it is because we don’t believe.

People Act on What They Believe

Knowing is not enough; acting is all that matters. You have to know before you can act. But what is the missing link between knowing and acting? It is belief.

Often I find myself in a season of poor eating. I love ice cream—a lot. And I like large lunches with heavy carbs. I’m not too fond of the blah feeling afterward, but the tastebuds get the better of my discipline.

Then I might read, “Eating vegetables and nuts for lunch will make you healthier, help you lose weight, and give you more energy and focus in the afternoon.”

Okay. Now I know. But reading that is not going to change my habits or desires.

I then listen to an audiobook like “Eat Fat, Get Thin” or “Fiber Fueled.” Rather than eight seconds to read a sentence about eating healthier, I’m listening to eight hours of the message. These books are full of testimonies, science, interesting facts, humor, and “ah-hah!” moments. And by the end, I not only know how to eat healthier. I want to!

I believe. And I can see how eating better would help me. I’m inspired to try. I want the benefits of it, and I believe they would work for me.

Then I hear that my business partner, Michael, has been eating salads for lunch every day for a couple of weeks. The testimony of his improved energy and focus adds additional belief. Now I don’t merely know. I believe. And I act.

I begin meal prepping. I add all the vegetables and toppings I need to the grocery order. Then, I chop up all the vegetables on Sunday so they can be ready to go. Next, I prepare my lunch salad for the next day. I create the base of baby spinach and load it up with a rotating mix of shredded carrot, broccoli, cauliflower, snap peas, multicolored bell peppers, and cucumber.

But let’s be honest. While all that is packed with micronutrients and vitamins, it doesn’t taste good. At all. Here’s the secret. You can make it taste good by adding healthy toppings.

I add a whole avocado to add rich taste and nutritious fat, and it nearly eliminates the need for dressing. Almonds, cashews, and walnuts give the salad a tasty crunch and provide protein and more healthy fats. Hardboiled eggs supply additional protein and a new texture. A bit of shredded chicken is all I need for a different taste, and I top it off with just a bit of cilantro avocado ranch dressing and some bacon bits. All the nutrition and so much flavor!

It tastes so good! I have so much more energy throughout the afternoon. I believed. And I acted. The actions reinforce the belief, and I keep acting. Life-changing.

First you know, then you believe, then you act.

This podcast is not about nutrition. So what does this have to do with financial planning?

There are four levels of belief regarding Financial Planning.

- When you know but don’t yet believe.

- When you know and believe.

- When you don’t know, but still believe.

- When no one can know, you still believe.

Level 1. When you know but don’t yet believe.

This level is the, “I know I should save more for retirement,” but you don’t yet honestly believe you should, and therefore don’t. You heard it once or twice. So you know it in the sense that you have accumulated that knowledge. But it has not translated into action.

A lot of people have this level of belief: none. They have amassed a lot of useful and useless financial information. They haven’t taken the time or hired someone to sift through the information and reorganize it in a plan of action that they can follow. People must push past this level of belief. More on that later.

Planning your finances so that you can see the relevant information and the effects and benefits of taking action can help push people into the second level of belief:

Level 2. When you know and believe.

This level is where educated decisions are made and action happens.

“I know that if I save $200 more per paycheck, I can reach my goal on the goal date. Time to change my 401(k) contribution.”

It’s full knowledge, mixed with some inspiration and motivation, that leads to action and success.

I know this level has been reached when meeting with a new client, and they say, “Ah! The thing is, I’ve always known I should do this. But when you put it that way, it makes so much more sense! I’ll get that done right away.”

This is one of the direct results of financial planning: knowledge, belief, and action. People already know a lot about many financial planning topics. But the planning moves them from level 1 to level 2. Then there are complex topics requiring that you move to level 3.

Level 3. When you don’t know, but still believe.

You cannot reach this level alone. You need someone to bring you there. Perhaps the requisite level of base knowledge has not been reached to fully understand a financial planning topic, even when presented by an author or planner skilled at simplifying concepts. This level is reached when you believe not in the message, but you believe the messenger.

“You know what, I don’t completely understand how this strategy is going to save us taxes over our lifetime. But I believe that if you say it will, it will.”

“I don’t understand all this legal jargon in this trust. But if you are telling me that it will do what we want, I believe you.”

Many people seek to understand a base level of finances and then act only on what they know and believe. Others seek greater expertise so that they can believe and act on levels they cannot know. This is often the complex intersections of investments, tax, estate, and retirement. The latter have decided that they can either do the 50-100 hours of reading required for them to know or delegate that to someone else and get actionable belief in 5-10 hours.

Levels 2 and 3 work together, allowing you to believe and act on the parts of your plan that you do and do not understand. If you can add the last layer, you can be unstoppable.

Level 4. When no one can know, you still believe.

Financial planning is all about planning for the future. No one knows the future. Thus, for many areas of planning, we cannot know that a strategy will work. But we can believe it.

For example:

“I don’t know when this recession will turn around. But I believe that it will because they always have.”

“I don’t know that equities will continue their permanent upward trend. But I believe that they will, as they always have.”

“I don’t know which investment plan will generate the best returns in the long run, but I believe mine will be good as any, better than most.”

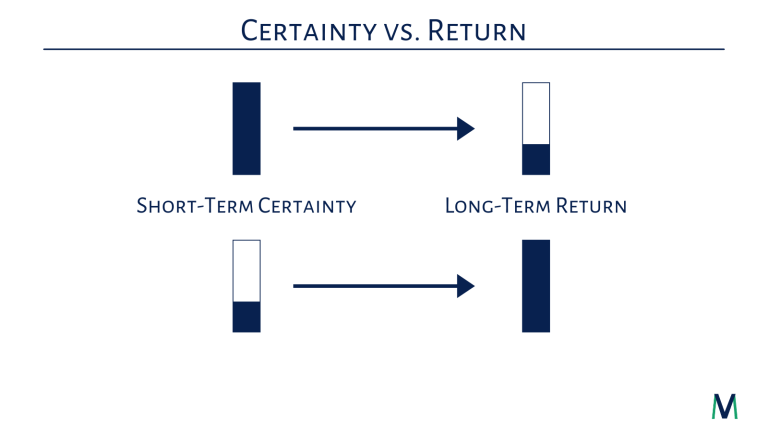

When it comes to planning, there is always an element of what Carl Richards calls “irreducible uncertainty.” Specific outcomes are unknowable, either by us or by anyone else. There is a level of uncertainty that we cannot overcome.

People will pay a lot of money for “certainty.” They pay this in the high fees of the financial products that offer a guarantee. But many who are selling certainty are ignoring the flip side of the coin. The more certainty you want in the short term, the more certainty you lose in the long run.

For example, you may purchase a fixed income annuity now because it now guarantees a certain income. Perhaps it even has a 2% inflation rider on it, so that the income will grow by 2% each year. That gives you some certainty now. But even if you ignore the fact that the current income will be lower than you could otherwise get without a guarantee, how certain are you that the 2% increase in the income will be sufficient? It will work as long as inflation averages 2% or less. But what if inflation grows to 3 or 4%? You have traded the uncertainty of equity returns for the uncertainty in the cost of living.

You cannot know. And neither can anyone else.

At some point, you will need to take some steps of faith. You will need to believe that an outcome will happen, even if we don’t know when or how. As Nick Murray puts it, “I do not know when things will turn out alright. I only [believe] that they will turn out alright.”

Historically, those who maintained belief in the face of irreducible uncertainty and stuck with a well-built plan have been rewarded.

It is time to start believing so that you can start acting. Reject level one: knowing and not believing. Embrace levels two through four.

Believe in what you already know. And act on it.

Believe in someone you can trust about strategies you don’t know, and act on them.

Believe in historically based future outcomes, which no one can know, and stick to the plan. That is how we succeed.

How do we begin believing? This leads to the final point.

You Can Build Your Belief

If you want to move from knowing a lot of randomness to believing and acting for your good and the good of your family, do these three things.

Isolate. Immerse. Invite.

1. Isolate and Follow One Strategy.

You cannot believe and do anything if you are constantly torn between opposing viewpoints.

It is similar to diets. This diet says to eat all the red meat I can because it’s packed with protein and numerous other benefits. That diet says to avoid red meat at all costs because it will give me cancer, among numerous other problems. Well, which is it! I guess I’ll keep eating the standard American diet.

In the same way, you can’t follow one strategy that tells you to pay off all your debt to cash flow your way to wealth and follow another that says to leverage your home and vehicles to invest the maximum amount. You can’t both continue to purchase additional permanent life insurance, and at the same time, buy term and invest the difference.

Pick one strategy and follow it, to the total exclusion of all others. You cannot believe in conflicting strategies. It is why this podcast will remain devoted to one strategy, as we discussed in the introduction episode.

If you are going to do this, you’ll want to make sure it works, is comprehensive, and comes from a minimally conflicted source.

If you are going to be entirely devoted to one strategy, it has to work. This idea is evident on the face. But how do you know if the strategy works?

You can look to see if it has worked for others. You can look to see if it has worked historically. And you should always be looking at the long-term efficacy.

It doesn’t matter who is winning the football game at the end of the first quarter. It is nice to be winning, sure. But the only thing that matters is who is winning at the end of the fourth quarter. It does not matter if the strategy seems excellent in the next few years. What matters if it is still working on the day you die.

It should be comprehensive. Not that you need to do everything at once, nor should you. But the strategy should eventually cover all areas of financial planning. You may have a good investment plan, but what about tax planning? Insurance planning? You may be able to tack a few plans together, but then you run back into the problem of them not working well together or even conflicting.

And your strategy should come from a source that has relatively low conflicts of interest. The degree to which the plan will work is inversely correlated with the source’s conflicts of interest.

Now, it is not possible to eliminate conflicts of interest. That is a fallacy, and we will cover it more in-depth in a later episode. I’ve heard several people claim, for example, that they follow Dave Ramsey because he doesn’t have any conflicts of interest. But that isn’t true.

He gets paid by advertisers every time you listen to the show, when you buy his books or his classes, when you sign up for his “Endorsed Local Provider” or “Smart Vestor Pro” programs, and when you take out a mortgage or life insurance through his recommended companies. It is in Dave’s best interest to have you continue buying his products, listening to his shows, and using his recommended products. Dave has a conflict of interest.

Thankfully, is the alignment of interests completely overshadows conflicts. It isn’t that he has no conflicts. He simply has low conflicts.

Imagine you have $500 per month to put toward something. You have Dave Ramsey on one side of the table, telling you to buy term and invest the difference in a Roth IRA. Maybe you go through one of Dave’s recommended investment advisors. And he will make a few bucks if you go through his recommended insurance brokerage. But you will maybe spend $50/m on the term insurance, and I struggle to see Dave’s company making more than $150 on his recommendations.

Imagine that you have a financial services representative for a mega life insurance company on the other side of the table. He recommends you put $40 toward term insurance, $260 toward whole life insurance, and $200 toward a Roth IRA. He has explained how “the stock market is very risky” and that the whole life has guaranteed cash value growth.

Who do you believe? Look at the source’s conflict of interest. Dave may make $150. The Financial Services Rep will likely make between $1,800 and $2,500 on just the insurance. He makes 10 to 100 times more in the first year on insurance than he would on the Roth IRA, depending on how he gets paid on both. They both have conflicts of interest. The levels of conflicts are miles apart.

Now let me make this next point quite clear. I am not advocating that you always choose the DIY cheap options and never pay for professionals. There are enough podcasts, articles, and books out there already advocating that everyone should be a DIYer because of all the money they could save. But here is where advice falls short for many.

Action. It never gets done.

I cannot tell you the number of people in my planning practice that, after we finally finish their estate planning and they have the will and all other documents completed, turn to me and say, “We’ve been meaning to do that for years.”

Let’s go back to our Ramsey vs. Insurance Salesmen. Imagine Dan and Bill have heard both arguments from both sides. Dan likes Dave Ramsey’s advice, and Bill is convinced by the “risky market” conversation and goes with the rep’s plan.

Two months later, they both die. Bill’s family gets paid out an enormous tax-free death benefit, ensuring they are cared for financially. Dan did invest the difference into his Roth IRA. But he never got around to the “buy term” part of the equation. Dan’s family gets the $900 that he has put into his Roth IRA so far, and nothing else. They proceed to weather the hardest years of their life, both emotionally and financially. But at least they never bought a whole life policy, right?

Look at the conflicts of interest. All else being equal, choose the lower conflicts. But also choose a strategy you will actually do. If that means paying a professional to help you get it done, do it.

To build your belief, you must isolate and follow one strategy. The strategy should work, be comprehensive, and the source should have relatively low conflicts of interest.

2. Immerse Yourself in the Strategy

Regularly consume content that supports and reinforces the strategy. Read books that align. Listen to podcasts that conform. Continually remind yourself that the strategy you are following is the right one. Do not stray from it or be lead astray. Saturate your mind with this one good strategy. It is the primary way you build your belief.

In Christianity, there is a massive emphasis on belief. Knowing God does not make people a Christian. They must believe. And they must continue to build that belief.

Followers of Jesus are encouraged to regularly read the Bible, pray, and belong to a church community. There is an initial belief in Jesus that makes one a Christian. But for people whose relationship is vital to them, they know that they need to make it a priority. Their belief will wane under the deluge of opposing worldviews. The only way to maintain the faith that richly adds to their life is to immerse themselves in the scripture, prayer, and a like-minded community.

The same is true for a financial strategy. It isn’t enough to believe in it once. You must reinforce and build that belief. And the best way to do that is to immerse yourself in it.

This podcast aims to do that. To help immerse you in a cohesive strategy that has historically worked, so you can continue to believe in and act on that plan moving forward. Subscribe to the podcast so that you can continue to build your belief.

A diet does not work if you only stick to it for a week. And a financial strategy doesn’t work if you only stick to it for a year. Indeed, some strategies don’t work until you’ve stuck with it for decades! It is incredibly un-human to stick to something alone for that long. For this reason, we need continual reinforcement of the strategy and help along the way.

Dave Ramsey has probably done this better than anyone. His signature book, The Total Money Makeover, has inspired millions. His class, Financial Peace University, has changed the lives of millions more. And his radio show, The Dave Ramsey Show, has reinforced the beliefs of listeners for decades.

I highly recommend all of them. Dave’s strategy works, has minimal conflicts of interest, and is relatively comprehensive. It will give the foundation that you need if you’ve never learned it and the ongoing belief to carry it out.

There are many aspects of his broad-based teachings that are only mentioned and not elucidated. This podcast, and proper financial planning, pick up where he leaves off. But I admire his ability to draw out and build belief in his listeners.

3. Invite an Accountability Partner

People stick to diets better when they have someone doing it with them. Crossfitters remain addicted to their gym because of the community there. People work through their typical human issues with the help of a therapist.

For something as crucial as your lifetime financial success, do not go it alone!

There will be times you lose faith. And in those times, you need someone who is resolutely steadfast to the plan. They will believe for you when you temporarily cannot. And when their steadfast belief carries you through, you will be grateful you did not attempt it alone.

Find someone who believes in the plan more than you do. Stick with them.

Isolate. Immerse. Invite.

Isolate and Follow One Strategy

Immerse Yourself in the Strategy

Invite an Accountability Partner

That is how you build belief that inspires action that changes lives.

Know. Then Believe. Then Act.

Stay tuned to this podcast to continue to build both your knowledge and belief.

Next episode, we cover the Four Horsemen, the behavioral mistakes we all make as humans that cost us half of our potential wealth over our lifetimes. It is essential that you both know and believe this one.

Subscribe so that it will automatically be in your podcast player next Monday.

If you have questions about this topic or any other topic, you can send an email to Questions@RetireMentorship.com. Or you can call us at 1-855-6-MENTOR (663-6867) and leave a voicemail. We will respond to you directly, and if we get the same question repeatedly, we’ll turn it into an episode.

Thanks for listening, and we will see you next week.

Want More? Become a RetireMember!

Get my book, 3D Retirement Income, for free, as well as access to live events, checklists and flowcharts, and wise counsel from one of the best minds in behavioral investing. Join today for free.

Need Help? Work with Me.

Schedule a Discovery Meeting with me through my Financial Planning firm, La Crosse Financial Planning. This no-cost, no-obligation conversation will determine what you are looking for and how we can help you retire successfully and stay successfully retired.

This article is educational only and is not intended to be investment, legal, or tax advice or recommendations, whether direct or incidental. Again, this is not investment advice. Consult your financial, tax, and legal professionals for specific advice related to your specific situation. Never take investment advice from someone who doesn’t know you and your specific situation. All opinions expressed in this article are those of the people expressing them. Any performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be directly invested in.